How To Buy A Home In Vancouver – What They Dont Tell You

When I first helped my client navigate the Vancouver real estate market, she thought the process would be straightforward. But after three months of house hunting, multiple offer situations, and unexpected closing costs totaling over $30,000, she realized buying a home in Vancouver is far more complex than most people imagine.

Buy a house in Vancouver, BC by getting mortgage pre-approval, hiring a local realtor, and reviewing recent comparable sales. Submit an offer with conditions for financing and inspection, complete due diligence, remove subjects, and close with a lawyer or notary. Budget for closing costs, taxes, and adjustments.

Vancouver’s housing market presents unique challenges that don’t exist elsewhere in BC. With the average home price hovering around $1.2 million and fierce competition from buyers across Canada, understanding this market isn’t just helpful—it’s essential for first-time home buyers and experienced purchasers alike.

Understanding the Vancouver Housing Market – Home Buying Process

Let’s be honest: the Vancouver housing market operates differently than anywhere else in Canada. Affordability challenges are well-documented in the City of Vancouver and throughout Metro Vancouver, but homeownership isn’t impossible. It requires strategic planning and realistic expectations about housing costs.

The market is characterized by limited supply, strong demand, and consistently competitive conditions. Many home buyers face multiple offer situations, requiring you to make an informed decision quickly. Understanding when to buy a house in BC can give you an edge – spring sees the most inventory, while winter offers less competition.

Step 1: Master Down Payment Requirements in BC

Your down payment represents the first step in the home buying process. In BC, the minimum down payment varies based on purchase price:

- Under $500,000: 5% minimum

- $500,000-$999,999: 5% on first $500,000, plus 10% on remainder

- $1 million+: 20% required

If you’re putting down less than 20%, you’ll need mortgage insurance, which adds to the total cost of purchasing a home. For first-time home buyers in BC, the Home Buyers’ Plan allows withdrawing up to $35,000 from your RRSP tax-free.

Understanding the distinction between deposit versus down payment is crucial. Your deposit (typically 5% of purchase price) is paid when making an offer, while your down payment is the total you’re contributing at closing. In addition to your down payment, budget breathing room for unexpected costs.

Many home buyers in Metro Vancouver use various programs for first-time buyers to help with their first home purchase.

Step 2: Calculate Monthly Mortgage Payments and Housing Costs

Most home buyers focus exclusively on purchase price, but your monthly mortgage payments tell the real affordability story. Beyond principal and interest payments to your lender, budget for:

Property taxes: Vancouver averages 0.25% of assessed value annually Home insurance: $1,000-$2,500 yearly for detached homes Maintenance: Budget 1-2% of your home’s value annually Strata fees: For condos and townhouses, expect $200-$800+ monthly

Lenders use the Gross Debt Service (GDS) ratio – housing costs shouldn’t exceed 32-39% of gross monthly income. They’re assessing how much they’re willing to lend based on what you need to pay monthly, requiring a down payment that keeps your GDS within acceptable limits.

Higher interest rates mean lower borrowing power. A mortgage broker can help you find the best rate, potentially saving thousands on monthly payments. Whether you’re buying a condo or detached home, understanding your true monthly mortgage obligation prevents financial stress.

Step 3: Secure Mortgage Pre-Approval Before House Hunting

Obtaining a mortgage pre-approval is a critical step in the home buying process that first-time buyers often overlook. A mortgage pre-approval shows sellers you’re serious and gives you a clear understanding of your budget.

Pre-approval typically requires proof of income, down payment confirmation, and credit checks. Your lender assesses how much they’re willing to lend based on your financial profile. Most pre-approvals hold your interest rate for 90-120 days, protecting you if rates rise.

Working with a mortgage broker often provides more options than going directly to banks. They can find specialized products for your unique situation, whether you’re a first-time homebuyer or purchasing your dream home.

Step 4: Choose Your Neighbourhood Strategically

Vancouver isn’t one market—it’s dozens of distinct neighbourhoods in Metro Vancouver. Your neighbourhood choice impacts lifestyle and investment returns. When evaluating areas, consider transit access, schools, and future development plans.

Popular Metro Vancouver locations each offer distinct advantages:

- North Vancouver: Mountain access, family-friendly atmosphere

- West Vancouver: Prestigious addresses, waterfront properties

- Burnaby: Central location, excellent transit, more affordable

- Richmond: International amenities, proximity to airport

The best neighbourhoods in Vancouver vary based on whether you’re buying a townhouse, condo, or detached home. Properties near transit typically command higher prices but offer better resale value.

Step 5: Understand Total Closing Costs

Here’s where many buyers experience sticker shock. Closing costs in BC typically add 3-5% to your purchase price. On a $1 million Vancouver home, that’s an additional $30,000-$50,000.

Property Transfer Tax (PTT): The largest closing cost for most buyers:

- 1% on first $200,000

- 2% between $200,000-$2 million

- 3% over $2 million

First-time buyers may qualify for the BC Property Transfer Tax exemption, saving up to $8,000. This partial rebate helps first time home buyers enter the market.

Legal fees: Budget $1,500-$3,000 for your real estate lawyer. Legal fees for buying in BC vary by transaction complexity but are essential.

Home inspection: $400-$800. Hiring a qualified home inspector protects your home purchase from costly surprises.

Title insurance: $250-$400 for one-time protection

If you’re buying a condo, review strata documents carefully. Whether you’re buying new construction or resale, understanding what taxes you pay prevents surprises. New homes include 5% GST, though rebates exist for properties under certain thresholds.

Step 6: Partner With a Real Estate Team

While you can buy without a realtor, navigating Vancouver’s competitive market without a buyer’s agent puts you at a disadvantage. A skilled real estate team brings market knowledge and negotiation expertise.

In BC, you’ll likely sign a buyer’s agent agreement outlining representation terms. Your agent should help you search for homes, understand the buying process, and give us a call when you find the perfect home.

Top agents excel at real estate negotiation, crucial when you need to negotiate in multiple offer situations. They help you navigate from open houses through to receiving the keys.

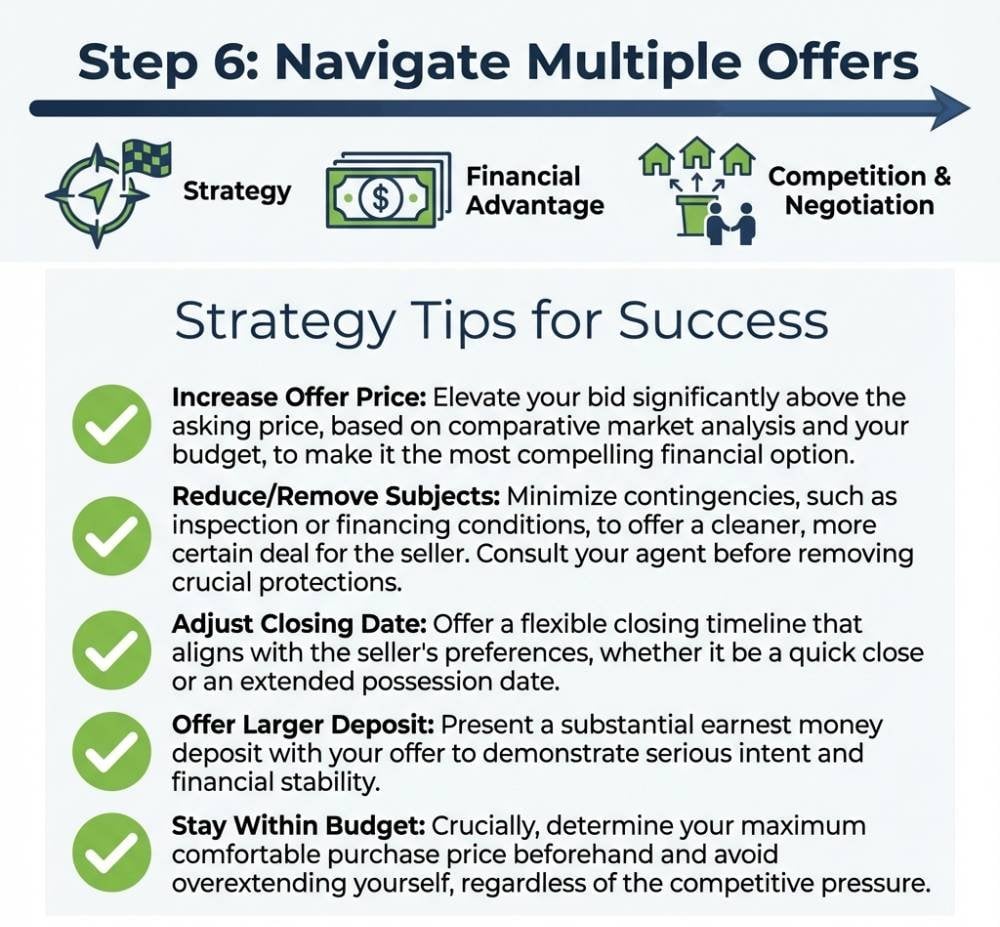

Step 7: Navigate Buying a Home in Vancouver and Making an Offer

The home search typically requires viewing 10-15 properties before finding your ideal match. Use a house hunting checklist to evaluate each property systematically against must-haves.

When ready to make an offer, your agent helps determine appropriate price and terms. In Vancouver, you’ll often encounter multiple offer situations where the seller receives several competing bids. Understanding how to make an offer in BC is crucial for success.

Your offer includes:

- Purchase price: Based on comparable sales

- Deposit: Usually 5%, held in trust

- Conditions: Financing, inspection, reviewing documents

- Completion date: When you receive the keys, typically 30-90 days

In the Fraser Valley and throughout Metro Vancouver, sellers often receive multiple offers. Winning in competitive situations requires strategy. Some buyers offer subject-free, but subject-free offers carry significant risk.

When buying a property, using a calculator can help determine your initial offer. Most experts suggest offering between 1.5 to 5 percent below the asking price, though in competitive markets, less than 20 percent under is more realistic. You’ll also need to consider comparable sales and market conditions. Consult a comprehensive guide to buying a home for detailed strategies on making successful offers.

Step 8: Complete Your Home Inspection

Once your offer is accepted, you typically have 5-10 days for due diligence. A professional home inspection is non-negotiable. The inspector evaluates structural integrity, mechanical systems, and potential issues.

For condos and townhouses, thoroughly review strata documents. Look for special levies, pending litigation, or insufficient reserves. Your lawyer conducts a title search verifying the seller owns the property.

During this period, you can still walk away if conditions aren’t satisfied. Once you remove subjects, you’re legally committed to completing the purchase. This step in the home buying process protects your interests.

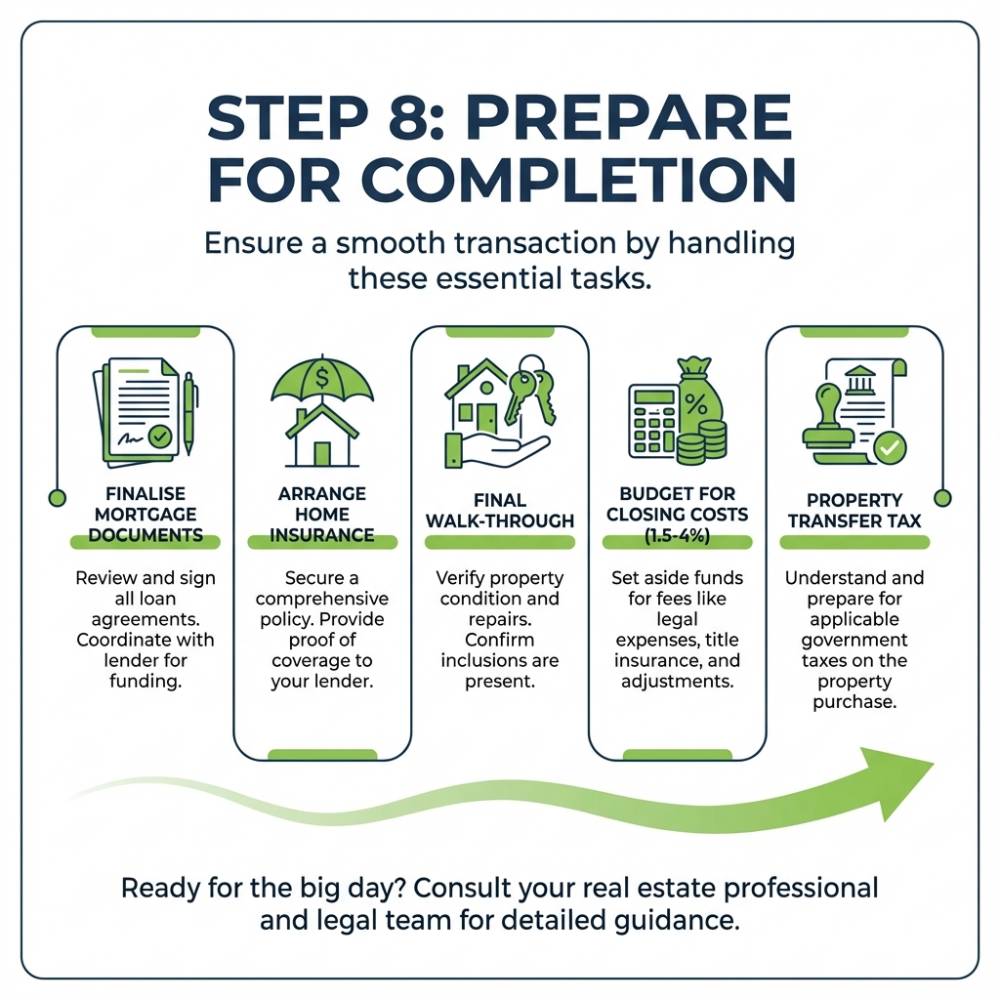

Step 9: Finalize Mortgage and Prepare for Closing

After subject removal, several weeks of work happen before possession. Your lender requires an appraisal confirming the property’s value supports your mortgage amount. If appraisal comes in low, you may need to renegotiate or increase your down payment.

Your lawyer will:

- Prepare closing documents

- Calculate adjustments for property taxes and fees

- Arrange title transfer and mortgage registration

You’ll need to:

- Complete a final walkthrough

- Arrange home insurance (required for completion)

- Book movers and arrange utilities

- Provide certified funds for down payment and closing costs

Understanding what happens on closing day sets proper expectations. You’ll receive keys late afternoon once funds transfer and title registers in your name.

Affordability Breakdown by Property Type in The Vancouver Real Estate Market

Vancouver offers various property types, each with distinct price points:

Detached houses: The average price exceeds $2 million in Vancouver proper, though more affordable options exist in surrounding areas of Metro Vancouver.

Townhouses: A middle ground offering land ownership. Townhouse resale value remains strong, making them popular with families seeking more space within your budget.

Condos: The most accessible entry point. When buying a condo, pay attention to strata fees, building condition, and rental restrictions. The average condo size in Vancouver is shrinking, but prices remain high.

Pre-construction vs resale: Comparing pre-construction and resale reveals trade-offs. Pre-construction offers customization but requires waiting years. Resale properties allow immediate occupancy.

Common First-Time Buyer Mistakes

After helping hundreds of homebuyers, I’ve seen these mistakes repeatedly:

Maxing out your budget: Just because a lender is willing to lend a certain amount doesn’t mean you should spend it all. Leave breathing room for life’s unexpected costs.

Ignoring total costs: Focus on monthly payments, not just purchase price. An average home with high strata fees costs significantly more than one with lower fees.

Making emotional decisions: Knowing if a house is right requires balancing emotion with practical analysis of the property type, location, and costs.

Waiving inspection: While removing conditions can win in competitive situations, it carries enormous risk. Always protect your home purchase with proper due diligence.

Essential Vancouver-Specific Considerations

Several unique factors affect Vancouver home buyers:

Speculation and vacancy tax: Properties must be your principal residence to avoid additional taxes. The BC speculation tax affects some buyers.

Foreign buyer restrictions: The Canada foreign buyer ban prevents many non-residents from purchasing property.

High overall costs: Understanding why Vancouver real estate is expensive helps set realistic expectations. Limited land, strong demand, and geographical constraints drive prices.

Buy versus rent: Given high prices, many wonder about buying versus renting in Vancouver. This depends on your financial situation and long-term plans.

Your Path Forward

Buying a house in Vancouver requires preparation, patience, and strategy. Understanding the home buying process – from calculating the 1.5% rule for maintenance costs to navigating the complexities of purchasing a property in Metro Vancouver – positions you for success.

How long it takes to buy a house in BC varies dramatically. Some buyers find their dream home within weeks; others search for months before finding the right property at the right price.

Whether you’re a first-time buyer or experienced homeowner, help you navigate this complex market by following this roadmap. You’ll make an informed decision, avoid costly mistakes, and ultimately secure a property meeting your needs.

From understanding minimum down payment requirements to calculating monthly mortgage payments, from choosing the perfect neighbourhood to working with a knowledgeable real estate team – each step builds toward your goal of homeownership.

Your Vancouver home purchase is achievable with the right approach. Start by getting mortgage pre-approval, understanding your true budget, and partnering with professionals who can guide you through this journey. The dream of owning a home in one of Canada’s most beautiful cities is within reach.

Ready to buy a home in Vancouver? The process doesn’t have to be overwhelming when you have the right guidance. From understanding the local market to navigating financing options and closing deals, having an experienced realtor makes all the difference.

Contact Richard Morrison today to start your home buying journey. With expert knowledge of Vancouver real estate, Richard will help you find your perfect property and negotiate the best deal for your future.

Let's Chat! Looking for a REALTOR® who can exceed your expectations? Look no further than Richard Morrison! His mission is to serve without limit & provide solutions that cater to your core needs.

• 20+ Years of Experience

• Medallion Member

• RE/MAX Hall of Fame

Latest Properties Added

| Property | Size | Price | Date Listed |

|---|---|---|---|

| 5808 Olympic Street, Vancouver | 2,904 sqft | $3,198,000 | Jul 8, 2026 |

| 4606 11th Avenue, Vancouver | 3,640 sqft | $3,680,000 | Jul 7, 2026 |

| 8468 12th Avenue, Burnaby | 3,937 sqft | $2,499,000 | Jul 7, 2026 |

| 7965 Burnfield Crescent, Burnaby | 2,385 sqft | $1,798,000 | Jul 8, 2026 |

| 201-7428 Byrnepark Walk, Burnaby | 751 sqft | $619,000 | Jul 8, 2026 |

| 216-5355 Lane Street, Burnaby | 741 sqft | $635,000 | Jul 8, 2026 |

| 617-5983 Gray Avenue, Vancouver | 823 sqft | $928,000 | Jul 8, 2026 |

| 411-345 Lonsdale Avenue, North Vancouver | 967 sqft | $779,000 | Jul 8, 2026 |

| 420-5777 Birney Avenue, Vancouver | 1,105 sqft | $1,199,000 | Jul 8, 2026 |

| 2-1592 Nanton Avenue, Vancouver | 2,219 sqft | $2,980,000 | Jul 8, 2026 |

| 214-2190 7th Avenue, Vancouver | 720 sqft | $628,000 | Jul 8, 2026 |

| 413-128 8th Street, North Vancouver | 1,283 sqft | $1,050,000 | Jul 7, 2026 |

Start your search with Richard Morrison, Top Award Winning Vancouver Realtor

Contact Richard Morrison Top Vancouver Realtor today to find a Vancouver houses for sale and Vancouver condos for sale. Also check out Burnaby houses for sale or maybe Burnaby condos for sale. If you prefer North Shore, take a look at our listings in North Vancouver houses for sale and North Vancouver condos for sale.